Understanding Agency Billing In Insurance

INSURANCE

Introduction Of Agency Billing

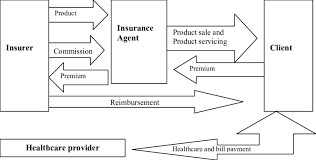

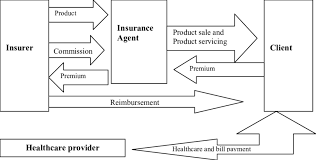

When it comes to the insurance industry, one of the key aspects to understand is agency billing. Agency billing refers to the process of an insurance agency collecting premiums from policyholders on behalf of the insurance company. This method of billing is commonly used in the industry and plays a significant role in the overall operations of insurance agencies. Agency billing refers to the process by which insurance agents or agencies collect and handle premium payments from policyholders on behalf of the insurance company. It involves the intermediary role of insurance agents in facilitating the payment transactions between the insured individuals or businesses and the insurance carrier.

Here's an example to illustrate agency billing:

1. Policy Purchase:

An individual or business decides to purchase an insurance policy and approaches an insurance agent for assistance.

The agent helps the client understand various policy options, coverage details, and premium costs.

2. Premium Calculation:

The insurance agent calculates the premium amount based on factors such as coverage limits, deductibles, and other relevant underwriting criteria.

3. Issuance of Policy:

Once the client agrees to the terms and decides to proceed, the insurance agent facilitates the issuance of the insurance policy from the insurance company.

4. Billing and Payment:

Instead of the policyholder dealing directly with the insurance company for premium payments, the agent bills the client for the premium amount.

The agent collects the payment from the policyholder, which may include methods such as checks, electronic funds transfer (EFT), or credit card payments.

5. Remittance to Insurance Company:

The insurance agent forwards the collected premium payments to the insurance company. This may occur at regular intervals, such as monthly or quarterly, depending on the arrangement between the agent and the insurer.

6. Commission and Fees:

In return for their services, insurance agents typically earn a commission from the insurance company for each policy sold. This commission is a percentage of the premium paid by the policyholder.

The insurance company may also charge the agent fees for administrative services.

7. Policy Maintenance:

The insurance agent continues to serve as the intermediary for any changes to the policy, endorsements, or updates. This includes handling renewals and addressing any policy-related inquiries from the client.

Importance of Agency Billing:

Agency billing is a crucial element in maintaining the financial stability of insurance agencies. It involves the collection of premiums from policyholders, which are then remitted to insurance carriers. This process ensures the sustainability of insurance agencies and the overall functioning of the insurance ecosystem.

The importance of agency billing in the insurance industry lies in the facilitation of premium payments and the overall management of customer relationships. Here are several key reasons why agency billing is significant:

1. Convenience for Policyholders:

Agency billing provides a convenient way for policyholders to manage their premium payments through their trusted insurance agents. This is particularly beneficial for individuals and businesses who prefer a personalized and direct relationship with their agents rather than dealing directly with the insurance company.

2. Enhanced Customer Service:

Insurance agents play a crucial role in providing customer service. By handling billing and payment processes, agents can address any questions or concerns that policyholders may have regarding their premiums, coverage, or policy details. This enhances the overall customer experience and satisfaction.

3. Smoother Premium Collection:

· Agency billing streamlines the premium collection process for insurance companies. Instead of dealing with individual policyholders for payments, insurers can rely on their network of agents to collect and remit premiums. This can lead to more efficient and organized financial transactions.

4. Personalized Guidance:

· Insurance agents often offer personalized guidance to policyholders, helping them understand the complexities of insurance policies, coverage options, and premium calculations. By being directly involved in the billing process, agents can reinforce this guidance and provide tailored advice to meet the specific needs of their clients.

5. Effective Policy Management:

· Agency billing facilitates effective policy management. Agents are well-positioned to handle changes to policies, process endorsements, and assist with renewals. This helps in maintaining accurate and up-to-date policy information, reducing the likelihood of errors or misunderstandings.

6. Commission Structure:

For insurance agents, agency billing is tied to their commission structure. Agents earn commissions based on the premiums collected, providing them with an incentive to actively engage in policy sales, renewals, and customer retention. This commission-based system helps align the interests of agents with the success of the insurance company.

7. Support for Diverse Payment Methods:

Insurance agents often accommodate a variety of payment methods preferred by policyholders, such as checks, electronic transfers, or credit card payments. This flexibility in payment options contributes to a positive customer experience.

8. Risk Mitigation:

Agency billing can help mitigate risks associated with non-payment or late payment of premiums. Agents can work closely with policyholders to ensure timely payments and address any financial challenges, reducing the likelihood of policy lapses.

Direct Billing vs. Agency Billing

There are two main methods of billing in the insurance industry: direct billing and agency billing. Let's explore the differences between these two approaches.

Direct Billing

In direct billing, the insurance company directly invoices the policyholder for the premium amount. The policyholder is responsible for making the payment directly to the insurance company. This method is commonly used for personal insurance policies, such as auto or homeowners insurance.

Direct billing offers convenience to the policyholder, as they receive the invoice directly from the insurance company and have the flexibility to choose their preferred payment method. It also allows the insurance company to have direct control over the billing process and ensures timely payment collection.

Agency Billing

Agency billing, on the other hand, involves the insurance agency collecting the premium amount from the policyholder and remitting it to the insurance company. In this case, the insurance agency acts as an intermediary between the policyholder and the insurance company.

Agency billing is commonly used for commercial insurance policies, such as those for businesses or organizations. It allows the insurance agency to provide additional services to the policyholder, such as policy administration, claims handling, and customer support. The agency may also offer different payment options to the policyholder, including installment plans.

. Here's a breakdown of the key differences between agency billing and direct billing:

1. Handling of Premium Payments:

Agency Billing: In agency billing, insurance agents or agencies collect premium payments directly from the policyholders. The agents then forward the collected premiums to the insurance company on behalf of the policyholders.

Direct Billing: In direct billing, policyholders make premium payments directly to the insurance company. The insurer manages the billing process and directly interacts with policyholders for payment transactions.

2. Intermediary Role:

Agency Billing: Insurance agents act as intermediaries between the policyholders and the insurance company. They play a central role in facilitating communication, managing billing inquiries, and handling premium transactions.

Direct Billing: There is no intermediary involved in direct billing. Policyholders interact directly with the insurance company for billing-related matters, including payment and policy administration.

3. Customer Relationship:

Agency Billing: The relationship between policyholders and insurance companies is often mediated and strengthened by the presence of insurance agents. Agents provide personalized service, guidance, and support throughout the policy lifecycle.

Direct Billing: Policyholders deal directly with the insurance company, which may result in a more direct but potentially less personalized relationship. Customer interactions are primarily with the insurer's customer service and administrative teams.

4. Commission Structure:

Agency Billing: In agency billing, insurance agents typically earn commissions based on the premiums collected. The commission is a percentage of the total premium paid by the policyholder.

Direct Billing: Since there is no intermediary in direct billing, there may be no commission paid to agents. Instead, the insurance company retains the entire premium amount, and any sales or administrative costs are managed internally.

5. Flexibility in Payment Methods:

Agency Billing: Insurance agents may offer flexibility in payment methods, accommodating various options such as checks, electronic transfers, or credit card payments based on the preferences of policyholders.

Direct Billing: The insurance company directly manages payment methods and options for policyholders. This may involve online payment portals, automatic bank transfers, or other methods determined by the insurer.

6. Risk Management:

Agency Billing: Agents can play a role in risk mitigation by actively working with policyholders to ensure timely payments and addressing any financial challenges that may arise.

Direct Billing: The insurance company directly manages and assumes the risks associated with premium collections, including the risk of non-payment or policy lapses.

Types of Agency Billing

Within agency billing, there are different types of billing arrangements that insurance agencies may offer to their policyholders. These include:

1. Direct Agency Billing

In direct agency billing, the insurance agency bills the policyholder directly on behalf of the insurance company. The agency collects the premium amount and forwards it to the insurance company, while also providing any necessary support and assistance to the policyholder.

2. Agency Bill with Direct Company Bill

This type of agency billing involves the insurance agency billing the policyholder for its own fees and commissions, while the insurance company directly bills the policyholder for the premium amount. The agency collects its fees separately from the policyholder and remits the premium payment to the insurance company.

3. Agency Bill with Company Reconciliation

In this arrangement, the insurance agency bills the policyholder for the premium amount and then reconciles the collected payments with the insurance company. The agency is responsible for ensuring that the premium amount is collected and remitted to the insurance company in a timely manner.

Understanding agency billing and the differences between direct billing and agency billing is essential for both insurance professionals and policyholders. It helps to ensure a smooth and efficient billing process, and provides clarity on the roles and responsibilities of the various parties involved.

In conclusion, agency billing is a fundamental aspect of the insurance industry, allowing insurance agencies to collect premiums on behalf of the insurance company. While direct billing involves the insurance company invoicing the policyholder directly, agency billing provides additional services and support through the insurance agency. Different types of agency billing arrangements exist to cater to the specific needs of policyholders and insurance agencies.

Summary

In summary, agency billing serves as a crucial link between policyholders and insurance companies, fostering positive customer relationships, providing support, and contributing to the overall efficiency of premium management in the insurance industry. Agency billing streamlines the premium payment process for policyholders by allowing them to make payments through their agents, who then manage the financial transactions with the insurance company. It also enables insurance agents to provide ongoing service and support to their clients throughout the life of the insurance policy